Basics of Personal Finance

Welcome to Sridhar’s newsletter number # 7. Appreciate you being here, so we can connect weekly on interesting topics. Add your email id here to get this directly to your inbox (https://sridhargarikipati.substack.com).

This is not a detailed notes unlike others as topic is about basics of personal financing and wanted to keep it in simple lines. Calling out at the basic level as this is how I kick start any new habits and I felt it’s easier to convey to someone else. Exercising is a best example in basics list I have. Eat simple and move more is my way of exercising. So for long run as basic as we keep certain things the more we will stick to it. Let’s begin,

Checking Account

Select an account which doesn’t have minimum balance requirements. If possible get one and take a one which can waive the fee if you deposit certain amount or your paycheck to it

Ensure you have access to Bank ATM always. Select a one, which is like universal , no fees for using any banks ATM

Account which gives you some interest is even better. Keep the funds in this account no more than 2 months of expenses in it.

Get the Amount out of this account, first thing as your paycheck gets deposited. So the amount which you meant to save is out of here first , so not to get spend

Certain number of free check books, mobile check deposit, online quick money transfer without fee’s ( As you will be Transferring to Saving Bank biggest chunk )

Savings Account

Open this account in different Bank than checking account

Select the one which has good web usage ( Applies to any account actually )

Allows to deposit money and withdraw money easy.

Normally withdrawal from these accounts takes 3 business days and they limit free withdrawals like 6 per month etc. These are savings money, so you won’t need often

Interest rates goes here and there always. So just pick which overall meets your criteria, don’t shuffle to new bank every time someone offers higher interest rate.

Again make sure no fees, minimum amount needed to maintain if possible. As you will start fresh or you may empty it for savings use it was intended for

Schedule auto transfer every month or per paycheck for deposits. Have a Auto Schedule enabled and have it first transaction of your checking account each month

Open multiple saving accounts per your needs or many banks allow to have subcategory of money in single account. Categorization helps you to be focus instead of looking at big number and taking all away for single saving expense.

Emergency Fund

Down payment for new home

Yearly Vacation

Education Fund

Vehicle Purchase ( Car )

Fiscal End Tax Payments, Like Insurance, Income Tax, Property Tax for Home etc.

Retirement savings ( Number One Priority among savings , Just calling out as its saving element which needs more growth than just sitting in savings account )

Yearly Gifts

Also ensure your bank is insured for your money, like in U.S we have FDIC (Federal deposit Insurance Corporation). Ex: if Bank fails, 250,000 USD is covered always.

Don’t just store your money, make it grow is basic principal of Savings and Investment accounts.

Credit cards

Skip this section if you are from country where credit rating doesn’t matter. In U.S home loans, car loans, even cell phone postpaid plans, home rent lease are few of many examples where credit rating is often checked. So in U.S its must to own credit card to build right credit score.

Select a card which suits you, like cash back, travel, Business etc.

Do not take any store cards as shopping is just one of purchase over our budget

Cards comes with fine and fees. Card should be free to you and should be good as long as paid on time

Always pay the statement clean

The longer you maintain cards more the good

Do not have more than 3 cards, as maintenance would be difficult. If you some running home loan, student loan which is also included in rating check how well one is paying, In Such case own 2 Cards.

Do auto payments for cards to make sure to never miss a payment

For less usage card just make may one transaction in 3 months and pay. Close only when you are sure. The longer credit opened accounts that much is better for credit

Increase your credit limit as per your pay and budget expense

Budgeting - Conscious Spending

For detailed notes on budgeting, see my earlier post. Click here

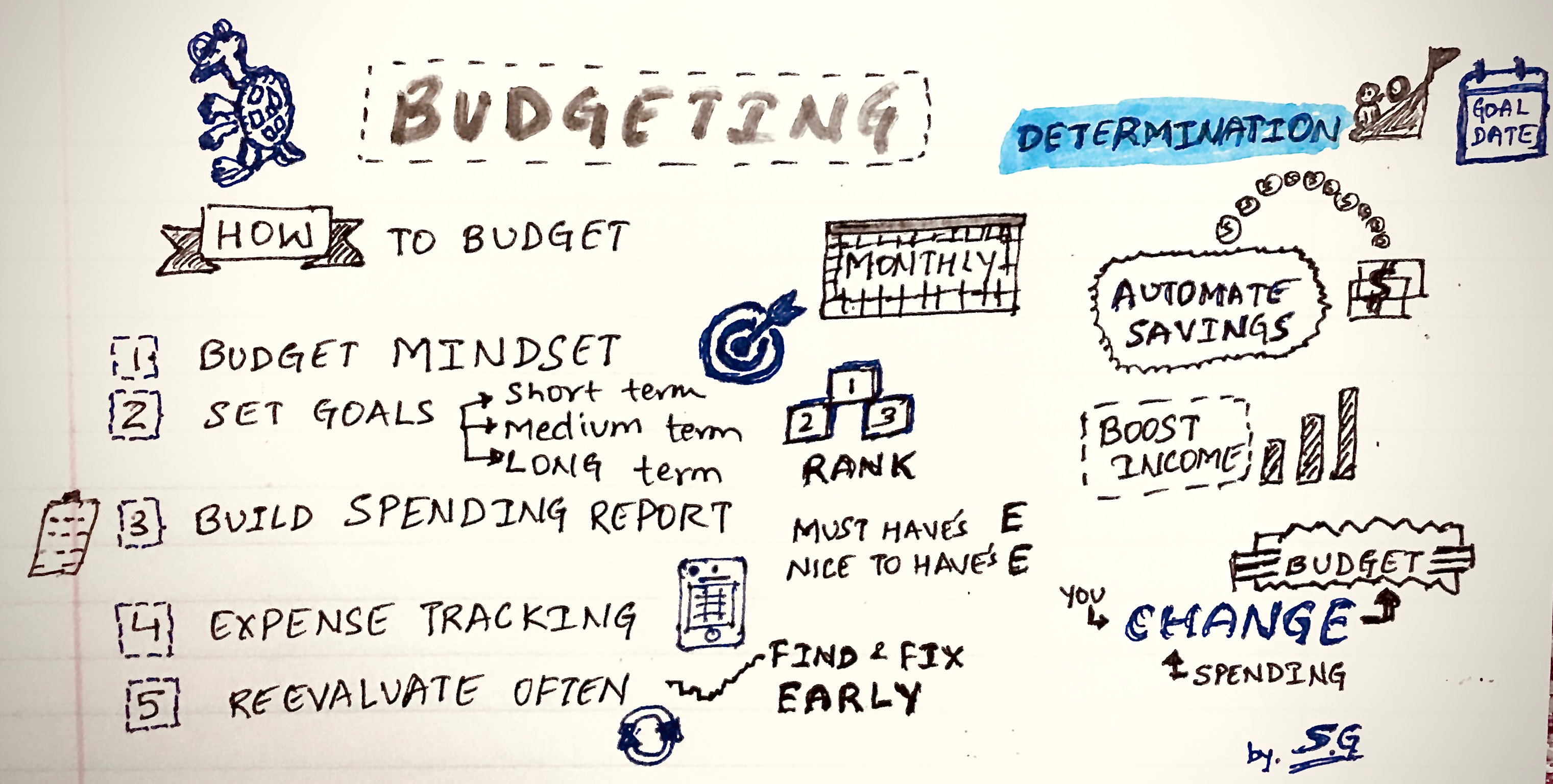

Here is the sketch notes from same post, adding it for reference as it conveys at high level. In personal finance we need to talk about budgeting for sure, it might sound boring topic but it’s one of the must to be on right path. Budgeting, savings etc. are just tools for us to handle money easier, so we can focus on other things in life

Look at your paycheck

Separate your needs vs wants

Build a spending report ( Break it down to every single dollar if its regular , like If you buy Morning Coffee daily )

Do Expense Tracking - Use Apps to help or Be old style with log book

Re-Evaluate Often - Find gaps and fix early

Budget, fine tune it. Once you know what is must and nice to have. You can keep budget aside, as you will be spending in your routine.

As you grow old, Your Expenses changes, so do work on increasing income, So does make your budget fit again

Once we master this, no need to track anymore, but if you see that spending is going in different way, then do come back to budgeting and get your spending, savings etc. on right path

You can also refer my Newsletter 4, where I talked about Frugal Lens vs Value Lens on Spending. Click here

Investing

As I have worked in India and currently working in USA, I want to share few of investing notes referring to both countries. As this post is also for my future reference to quickly go over.

Before we get into Investing,

Make sure No Debt is there (Home Loan is fine as its long term )

Emergency fund is setup for 6-9 months

Have a saving fund set aside for your wedding or upcoming baby in your life or Pregnancy-delivery medical bills (These are your expenses which you will spend, based on how near term they are, do have this money invested in a way so you can get it out. These are examples but everyone will have some known expense coming up in near term so planning for it is needed instead of no plan.

Retirement Savings is top one priority in investment, as it should begin early in life to gain long term benefits when you retire. When it comes to retirement there won’t be any loans given out neither we will have paycheck, so you have to plan this with higher preference.

Open a 401(K) account if your employer gives a match. See what funds they offer, if they are like Vanguard Target Date funds , then max out. If No Employer match, only deposit some small % to take tax benefit. Else ignore this

This is same as Employee Provident Fund (EPF) in India. Do join a company always who participate in EPF, provides Life Insurance, medical Insurance for family, discounted parental insurance. Ignore the companies who won’t provide these basics.

Open a Roth IRA Account and invest money in it. Do note, you deposit money to your account and also needs to invest to get its gains. Banks also gives a IRA in CD ( Certificate of Deposit ) form which have almost same as savings bank interest rate, So it’s worth to open a brokerage firm like Vanguard or others so can invest in market

This is like 80C savings we do in India, where we open fixed deposit for 5 years (to get tax benefit for that year), LIC Money back policy etc. In both cases actual amount deposited is not taxed, but gains are taxed on withdrawal time.

This is must, as we get current year tax benefit

If your employer has HSA Insurance, then do opt for it. Everyone has medical expenses even you don’t have right now, you are saving the amount before tax. Unlike 401(k), you can withdraw for medical bill payments.

Also, Use HSA Account for Investing. Most of them allows to invest in mutual funds, ETFs or even individual stocks.

I strictly say no to Mutual funds. In India especially this is marketed a lot over web and TV. Know the fee’s they really eat up a long term. Don’t go with advertising, run the numbers always.

Invest in Target date funds as first priority in market. Vanguard 2055 (Retirement Year) etc. are examples. Yes, they have fees, but look for brokerage having lowest fee. Target date funds are guaranteed to give return over long term.

Invest in Index fund as second choice. This allows to invest in multiple companies, ex: S&P 500 is index of performance of the 500 largest U.S. public companies. Individual company stock can go up and down, but entire industry is hard to go down.

Individual Stocks - Only Luck, winning at them is pure luck. So chance of failing is lot. Invest in sector or company whose business you understand and really see a future growth. If you don’t know how process of they running a business, then stay away from being their shareholder.

These are just above to get started in investing. Rather being in fear and holding cash, do invest the money. As economy is not going be same, today’s cash value is not going to be same after a decade or at the 3 decades after you plan to retire.

Irrespective of choice of investing, Do Diversify

Invest in Gold, 15% cash amount max as FDIC is insured by bank

Don’t risk it. See where you are and remember your goals. So act accordingly.

Life Big Ticket Expenses & Planning

Education Fund - Do plan for this always. As re-skill will help you in long term future. If you need to learn something I recommend pick a good e-book. Don’t ever think about buying say 20$ book as even some advice will be helpful for you in long run. Have a plan if you have this as debt to clear it off

Wedding Expenses - You may think to get it done with just 2 of you. But you never know if you end up celebrating with larger audience. Even before you know it, this is going to be big check on your pocket. So better plan for this expense, rather than flushing out your all earned money so far and spending it over a week

Home Buying - this is one of the biggest expense in our life, so do plan for it.

Also, buying a home is not always a right choice in many markets. Don’t believe in renting is throwing a money. Do your market research and decide if renting or buying is a better choice. Here is an example of buy vs rent calculator by New York Times.

https://www.nytimes.com/interactive/2014/upshot/buy-rent-calculator.html

If renting is better for you, then do rent. Else do buy. Understand the home buying and maintenance process for sure before you get into biggest investment of your life. If you rent, than do make sure to invest rest of your money right.

That’s all for the basics. Do let me know in comments or reply me over email to share what’s your personal financing strategy, tips, advice.

If you like the newsletter, then do like and leave a comment by clicking below

Stay Connected, Share Ideas, Spread Happiness.