Budgeting

Welcome to week 3 of Sridhar’s newsletter. Appreciate you being here, so we can connect on interesting topics. If you haven’t subscribed yet, here is the link (https://sridhargarikipati.substack.com).

One of you mentioned that my email was not seen in your primary inbox of Gmail. You can move my email under promotions tab into Primary tab. By doing so, all future emails from me will be delivered to the Primary tab.

Sharing visual image of topic as quick note ahead.

This came as recommendation topic for me to write about. Do note, I’m not a financial consultant or have any financial degree to my name. Having knowledge on personal finance for sure helps one and I believe sharing such thing with others is good. necessity has triggered many times for me to create a budget plan and stick to it to achieve something. Saving monthly have been my norm but I did notice that when I really set a goal date and number to save and stick to budget it really helps to achieve it faster. I won’t be sharing any budget template as it really needs individual to come up with his own template and stick to it. If you just google around, you will find plenty of templates. Even a simple excel sheet is enough to put a budget plan and follow through. It just requires you and your determination to manage your finances.

I personally don’t believe that money can buy happiness but being financially independent and secure can for sure keep you healthy financially to focus on other things in life. As having some 9 months of expenses sets aside in case of job loss, it gives a security to look for next opportunity or Unexpected medical bill to be paid or even say planned educational fund for kids' future or retirement plan. In all these cases if one is financially stable, it's one of most important things to worry less. Spending is way easy and now a days everyone has championed it. Just look around, how much people are spending on Gadgets, Eating Out, fast fashion etc. Money is easily going to get away if one doesn’t know how manage personal finance.

Check this out by Ronny Chieng, perfectly saying how mindset is now a days over spending.

Hope you had the laugh, my point here how funny he is conveying today’s reality.

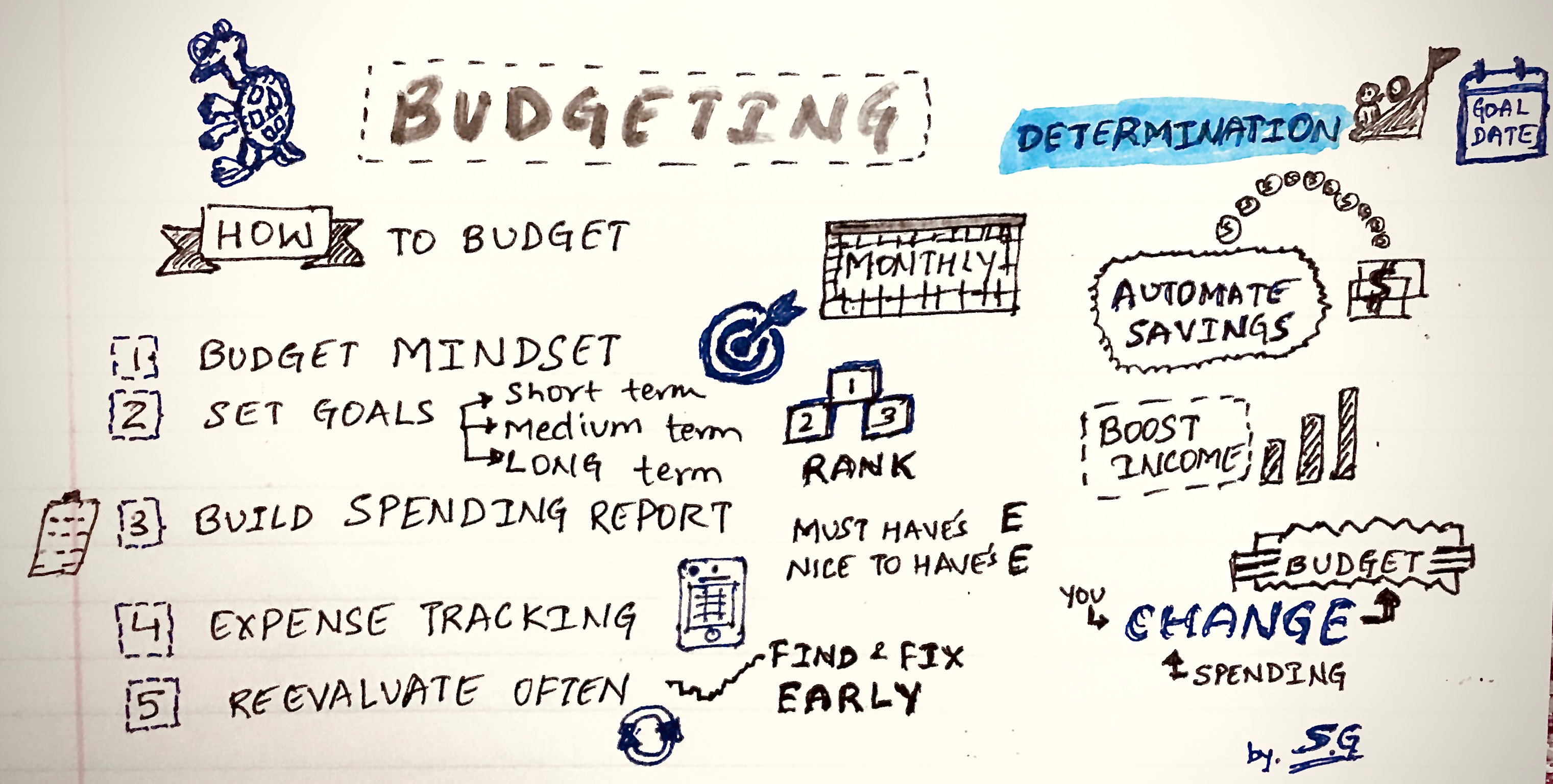

Get Ready - So first thing in budgeting is getting yourself ready. This isn't about the excel numbers you have kept together and getting it done for first time. Right Mindset is important. I’m not talking about budgeting at all here, I’m talking about as a person your overall mental and emotional state when it comes to living. It’s important to know yours and your family needs first. So, once you aware of it, you will know what’s must and what's nice to have. Knowing this margin is important, as it will help us to build the budget right, so it easier to stick to it. Rather than restricting yourself to some strict plan, impacting your lifestyle will eventually let it fail.

Goal - Set Optimistic Goal. That is, If your income is 3000$ per month, than its not expected to save each month 2500$.Once you will analyze the current state and make changes , than you will be in right position to know how much you can keep aside. This number will let you know by expecting which time, you can reach your budget goal.

Also, set your goal more accurate. Instead of saying, i want to clear my student loan, Set the goal as I want to clear my student loan in next 24 Months or Date would be more helpful say by Dec 31st, 2021. However small your plan is having a plan is worth it. As you never know the wealth you set aside will be useful some point of life. So even its a plan to buy yourself a Laptop or Down payment for Home, Retirement savings. Planning will always keep you ahead, then not planning at all. As today’s money won’t have same value in next 20 years. Also, your life is not going be same always, expenses goes up as we grow in our lifetime.

For this, I recommend having 3 goals always

Short Term (Example: Want to buy Laptop)

Medium Term (Example: Financing Kids Education)

Long Term (Example: Retirement Savings)

Also rank these goals accordingly. In above example Long term goal takes higher preference than medium term. As for Kids we can get an educational loan and kid can themselves as well clear it off later with their own income, but when it comes to retirement there won’t be any loans given out, So you have to plan this with higher preference.

Build Spending Report - First thing you must categorize your expenses.

Example:

Home & Utilities

Groceries

Dinning Out

Transportation

Shopping & Entertainment

Insurances

Taxes

Medical

Look back at your last one year of expenses to arrive at right expected numbers. The reason why i say an year because, i end up spending more money during summer as i go out more compared to coldest winter months. Knowing average helps a lot, to put the budget right. If this is the first time, start with your current expected numbers and come back every week once and look back at your expenses and re-adjust each category. You can go full analytics on budget if you like or even a simple excel few rows/columns is also sufficient. Important thing here is to understand your average spending , So you can come to realistic number to save each month or pay check as you get. ( Not everyone’s job pays monthly, few who make income doing services work get paid for each contract they finish. Once you gain the personal financing knowledge , Budgeting will come as ease to any category. )

Also, Spending report will help you re look at your expenses. Once you are aware what's yours must and nice to have, you can crunch the numbers. Spending is going to change as one move from bachelor to family person. So does incomes also need to move higher.

Income - As spending is going to change drastically as we move from 20’s to 30’s to 40’s so on. Boost your income, never settle to any job which keeps paying you same amount year after year. As economy is not going to be same as it is right now. If today you have income of 6k $ per month, than you would need approx 25k $ per month income after 25 years for living.

Working overtime as work need arise, so you can add more income

Pick up additional weekend work

Use your secondary skills to generate some income. Maybe you are good cook, start YouTube channel. Silly it sounds, you never know when your secondary skill will become your primary skill and your primary income source. Your primary day job may be forced upon you following society job path, sometimes re-looking at secondary job will push us to see outside of our day job and we may end up creating our own path.

Learn market hot skills, to boost your resume, to get you more income on your next job or get rise in current jobs.

If you are looking for more, i recommend reading some good “personal finance books “out there. Just google it, read at least couple of them to get an idea. Most of these are self-help when you are starting out and once you have your basics set follow some podcasts , take your notes from different perspectives so you have enough knowledge to alter rules as they meet your financial state.

As you add more income and if your needs of living don’t change much, don’t change your budgeting style. Living by your means is always good, consuming more is not going to help you. Intention here is to learn the personal finance skill and as you add these skills and add more money into your life. Take that freedom and work on other aspects of your life. Financial freedom will move your focus on what's important to you, instead of stressing about money. Say you got a Bonus this year, don’t spend this income outside of your budget. You learn these skills not to spend more, rather spend for your needs. Stick to your budget living and use this money for your future or make the money work for you - Invest to make more.

Expense Tracking - This is the hardest part of budgeting. You have set a budget, sticking to it without knowing margin for each bucket will easily leave money through the cracks. So do track the money initial few months. Routines will help you here, once you have established your monthly spending routine. Example, you visit groceries only once in 2 weeks. If you missed something it has to wait for its next visit. Routines will help a lot here to track the expense. Say instead of eating out every day at lunch, cook yourself a meal every day and weekly once go out to eat. form routines for every single spending category, so you buy as per your needs.

There are many smartphone apps out there to track expenses, Mint is the one i recommend. You can search others, just make it easy on you to track. Once you have routines formed, no need to track like this.

Mint: Personal Finance & Money

Re-evaluate Budget - You have already set up a budget. Do note there will many cases month to month where you will notice that you are slipping out of your budget. This is going to push your goal date as well. So, it's important to reevaluate your budget always. Currently, check your expenses and see what’s causing that bleed. If you underestimated something, do adjust the budget early in your timeline. So will have enough time down the line to add more income, add your bonus earned at work, add your saving bank interest amount etc. to get you on track again.

I personally do not believe when people say they cannot save money, their circumstances were different, or income is low. I have known personally people earning 15k INR per month as well saving money and few earning very high income of 200k USD per annum. Also seen where one even earning 90K INR per month also giving so many reasons as unable to save. So, stop complaining about the money, gain the knowledge and regain the information again and again as income, economy, standard of living changes as we grow old. Budget is must if you have debt, use it to clear it off. I’m not saying every debt is bad to get clear, there are good debts and bad debts. The Debts which you take for your education is good debt as you are investing in yourself and it will help future you to earn it back. Always run your numbers against the market rates and some cases even good debt is also good to clear it off if you are ahead of it.

Keep in your investment basics always handy, to remind yourself. As we go on budget journey, In the income part where we talked about generating additional income. It’s fine if you are making additional income without touching your saved income already. If you are using your saved money and investing in some real estate or stock market to generate additional income, then be cautious. I prefer to have an emergency fund in my case for 9 months. Ideally based on your current situation have an emergency funds around six to nine months range of expenses handy, before you get into investing using existing saved money. If you are a seasonal worker like wedding photographer , in current Covid-19 situation many events, parties are been cancelled so in such cases emergency fund should be set even higher for those type of progressions.

Don’t take budgeting as complex task, rather start small. Concentrate on categories which you first noticed as overflowing your budget. the slow pace will allow to master the budgeting. If you need help,

Do separate your spending account and saving account in different banks.

Automate your savings. on day 1 when your income gets credited, set auto transfer to move the expected saving fund to savings account at different bank

If you have lived below your budget, then treat that money as additional income and move it as well to saving account. Many have urge to spend it as winning over budget but do note it shows that you are learning on your budgeting way to live as per your needs. This win is not to celebrate by spending it out, rather add as booster to your goals.

Just hit me an email or phone call, we can brainstorm more on this topic. As budgeting is learnt better if we can talk real life examples as they inspire more. Happy budgeting :-)

Stay Connected, Share Ideas, Spread Happiness.